In this post ‘Practical Machine Learning with R and Python – Part 3’, I discuss ‘Feature Selection’ methods. This post is a continuation of my 2 earlier posts

While applying Machine Learning techniques, the data set will usually include a large number of predictors for a target variable. It is quite likely, that not all the predictors or feature variables will have an impact on the output. Hence it is becomes necessary to choose only those features which influence the output variable thus simplifying to a reduced feature set on which to train the ML model on. The techniques that are used are the following

This post includes the equivalent ML code in R and Python.

All these methods remove those features which do not sufficiently influence the output. As in my previous 2 posts on “Practical Machine Learning with R and Python’, this post is largely based on the topics in the following 2 MOOC courses

1. Statistical Learning, Prof Trevor Hastie & Prof Robert Tibesherani, Online Stanford

2. Applied Machine Learning in Python Prof Kevyn-Collin Thomson, University Of Michigan, Coursera

Check out my compact and minimal book “Practical Machine Learning with R and Python:Third edition- Machine Learning in stereo” available in Amazon in paperback($12.99) and kindle($8.99) versions. My book includes implementations of key ML algorithms and associated measures and metrics. The book is ideal for anybody who is familiar with the concepts and would like a quick reference to the different ML algorithms that can be applied to problems and how to select the best model. Pick your copy today!!

1.1a Best Fit – R code

The Best Fit requires the ‘leaps’ R package

library(leaps)

source('RFunctions-1.R')

df=read.csv("Boston.csv",stringsAsFactors = FALSE)

names(df) <-c("no","crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

df1 <- df %>% dplyr::select("crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

bestFit=regsubsets(cost~.,df1,nvmax=13)

bfSummary=summary(bestFit)

plot(bfSummary$rss,xlab="Number of Variables",ylab="RSS",type="l",main="Best fit RSS vs No of features")

a=which.min(bfSummary$rss)

points(a,bfSummary$rss[a],col="red",cex=2,pch=20)

![]() The plot below shows that the Best fit occurs with all 13 features included. Notice that there is no significant change in RSS from 11 features onward.

The plot below shows that the Best fit occurs with all 13 features included. Notice that there is no significant change in RSS from 11 features onward.

plot(bfSummary$cp,xlab="Number of Variables",ylab="Cp",type='l',main="Best fit Cp vs No of features")

b=which.min(bfSummary$cp)

points(b,bfSummary$cp[b],col="red",cex=2,pch=20)

![]() Based on Cp metric the best fit occurs at 11 features as seen below. The values of the coefficients are also included below

Based on Cp metric the best fit occurs at 11 features as seen below. The values of the coefficients are also included below

coef(bestFit,b)

## (Intercept) crimeRate zone charles nox

## 36.341145004 -0.108413345 0.045844929 2.718716303 -17.376023429

## rooms distances highways tax teacherRatio

## 3.801578840 -1.492711460 0.299608454 -0.011777973 -0.946524570

## color status

## 0.009290845 -0.522553457

plot(bfSummary$bic,xlab="Number of Variables",ylab="BIC",type='l',main="Best fit BIC vs No of Features")

c=which.min(bfSummary$bic)

points(c,bfSummary$bic[c],col="red",cex=2,pch=20)

![]()

plot(bestFit,scale="r2",main="Rsquared vs No Features")

![]() R has the following set of really nice visualizations. The plot below shows the Rsquared for a set of predictor variables. It can be seen when Rsquared starts at 0.74- indus, charles and age have not been included.

R has the following set of really nice visualizations. The plot below shows the Rsquared for a set of predictor variables. It can be seen when Rsquared starts at 0.74- indus, charles and age have not been included.

plot(bestFit,scale="Cp",main="Cp vs NoFeatures")

![]() The Cp plot below for value shows indus, charles and age as not included in the Best fit

The Cp plot below for value shows indus, charles and age as not included in the Best fit

plot(bestFit,scale="bic",main="BIC vs Features")

![]()

1.1b Best fit (Exhaustive Search ) – Python code

The Python package for performing a Best Fit is the Exhaustive Feature Selector EFS.

import numpy as np

import pandas as pd

import os

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression

from mlxtend.feature_selection import ExhaustiveFeatureSelector as EFS

df = pd.read_csv("Boston.csv",encoding = "ISO-8859-1")

df.columns=["no","crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status","cost"]

X=df[["crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status"]]

y=df['cost']

lr = LinearRegression()

efs1 = EFS(lr,

min_features=1,

max_features=13,

scoring='neg_mean_squared_error',

print_progress=True,

cv=5)

efs1 = efs1.fit(X.as_matrix(), y.as_matrix())

print('Best negtive mean squared error: %.2f' % efs1.best_score_)

print('Best subset:', efs1.best_idx_)

Features: 8191/8191Best negtive mean squared error: -28.92

## ('Best subset:', (0, 1, 4, 6, 7, 8, 9, 10, 11, 12))

The indices for the best subset are shown above.

1.2 Forward fit

Forward fit is a greedy algorithm that tries to optimize the feature selected, by minimizing the selection criteria (adj Rsqaured, Cp, AIC or BIC) at every step. For a dataset with features f1,f2,f3…fn, the forward fit starts with the NULL set. It then pick the ML model with a single feature from n features which has the highest adj Rsquared, or minimum Cp, BIC or some such criteria. After picking the 1 feature from n which satisfies the criteria the most, the next feature from the remaining n-1 features is chosen. When the 2 feature model which satisfies the selection criteria the best is chosen, another feature from the remaining n-2 features are added and so on. The forward fit is a sub-optimal algorithm. There is no guarantee that the final list of features chosen will be the best among the lot. The computation required for this is of  which is of the order of

which is of the order of  . Though forward fit is a sub optimal solution it is far more computationally efficient than best fit

. Though forward fit is a sub optimal solution it is far more computationally efficient than best fit

1.2a Forward fit – R code

Forward fit in R determines that 11 features are required for the best fit. The features are shown below

library(leaps)

df=read.csv("Boston.csv",stringsAsFactors = FALSE)

names(df) <-c("no","crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

df1 <- df %>% dplyr::select("crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

train_idx <- trainTestSplit(df1,trainPercent=75,seed=5)

train <- df1[train_idx, ]

test <- df1[-train_idx, ]

fitFwd=regsubsets(cost~.,data=train,nvmax=13,method="forward")

valErrors=rep(NA,13)

test.mat=model.matrix(cost~.,data=test)

for(i in 1:13){

coefi=coef(fitFwd,id=i)

pred=test.mat[,names(coefi)]%*%coefi

valErrors[i]=mean((test$cost-pred)^2)

}

plot(valErrors,xlab="Number of Variables",ylab="Validation Error",type="l",main="Forward fit RSS vs No of features")

a<-which.min(valErrors)

print(a)

## [1] 11

points(c,valErrors[a],col="blue",cex=2,pch=20)

![]() Forward fit R selects 11 predictors as the best ML model to predict the ‘cost’ output variable. The values for these 11 predictors are included below

Forward fit R selects 11 predictors as the best ML model to predict the ‘cost’ output variable. The values for these 11 predictors are included below

coefi=coef(fitFwd,id=i)

coefi

## (Intercept) crimeRate zone indus charles

## 2.397179e+01 -1.026463e-01 3.118923e-02 1.154235e-04 3.512922e+00

## nox rooms age distances highways

## -1.511123e+01 4.945078e+00 -1.513220e-02 -1.307017e+00 2.712534e-01

## tax teacherRatio color status

## -1.330709e-02 -8.182683e-01 1.143835e-02 -3.750928e-01

1.2b Forward fit with Cross Validation – R code

The Python package SFS includes N Fold Cross Validation errors for forward and backward fit so I decided to add this code to R. This is not available in the ‘leaps’ R package, however the implementation is quite simple. Another implementation is also available at Statistical Learning, Prof Trevor Hastie & Prof Robert Tibesherani, Online Stanford 2.

library(dplyr)

df=read.csv("Boston.csv",stringsAsFactors = FALSE)

names(df) <-c("no","crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

df1 <- df %>% dplyr::select("crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

set.seed(6)

nvmax<-13

cvError <- NULL

for(i in 1:nvmax){

noFolds=5

folds = sample(1:noFolds, nrow(df1), replace=TRUE)

cv<-0

for(j in 1:noFolds){

train <- df1[folds!=j,]

test <- df1[folds==j,]

fitFwd=regsubsets(cost~.,data=train,nvmax=13,method="forward")

coefi=coef(fitFwd,id=i)

test.mat=model.matrix(cost~.,data=test)

pred=test.mat[,names(coefi)]%*%coefi

rss=mean((test$cost - pred)^2)

cv=cv+rss

}

cvError[i]=cv/noFolds

}

a <- seq(1,13)

d <- as.data.frame(t(rbind(a,cvError)))

names(d) <- c("Features","CVError")

#Plot the CV Error vs No of Features

ggplot(d,aes(x=Features,y=CVError),color="blue") + geom_point() + geom_line(color="blue") +

xlab("No of features") + ylab("Cross Validation Error") +

ggtitle("Forward Selection - Cross Valdation Error vs No of Features")

![]() Forward fit with 5 fold cross validation indicates that all 13 features are required

Forward fit with 5 fold cross validation indicates that all 13 features are required

a=which.min(cvError)

print(a)

## [1] 13

coefi=coef(fitFwd,id=a)

coefi

## (Intercept) crimeRate zone indus charles

## 36.650645380 -0.107980979 0.056237669 0.027016678 4.270631466

## nox rooms age distances highways

## -19.000715500 3.714720418 0.019952654 -1.472533973 0.326758004

## tax teacherRatio color status

## -0.011380750 -0.972862622 0.009549938 -0.582159093

1.2c Forward fit – Python code

The Backward Fit in Python uses the Sequential feature selection (SFS) package (SFS)(https://rasbt.github.io/mlxtend/user_guide/feature_selection/SequentialFeatureSelector/)

Note: The Cross validation error for SFS in Sklearn is negative, possibly because it computes the ‘neg_mean_squared_error’. The earlier ‘mean_squared_error’ in the package seems to have been deprecated. I have taken the -ve of this neg_mean_squared_error. I think this would give mean_squared_error.

import numpy as np

import pandas as pd

import os

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression

from sklearn.datasets import load_boston

from mlxtend.plotting import plot_sequential_feature_selection as plot_sfs

import matplotlib.pyplot as plt

from mlxtend.feature_selection import SequentialFeatureSelector as SFS

from sklearn.linear_model import LinearRegression

df = pd.read_csv("Boston.csv",encoding = "ISO-8859-1")

df.columns=["no","crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status","cost"]

X=df[["crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status"]]

y=df['cost']

lr = LinearRegression()

sfs = SFS(lr,

k_features=(1,13),

forward=True,

floating=False,

scoring='neg_mean_squared_error',

cv=5)

sfs = sfs.fit(X.as_matrix(), y.as_matrix())

a=sfs.get_metric_dict()

n=[]

o=[]

for i in np.arange(1,13):

n.append(-np.mean(a[i]['cv_scores']))

m=np.arange(1,13)

fig1=plt.plot(m,n)

fig1=plt.title('Mean CV Scores vs No of features')

fig1.figure.savefig('fig1.png', bbox_inches='tight')

print(pd.DataFrame.from_dict(sfs.get_metric_dict(confidence_interval=0.90)).T)

idx = np.argmin(n)

print "No of features=",idx

b=list(a[idx]['feature_idx'])

print(b)

print("Features selected in forward fit")

print(X.columns[b])

## avg_score ci_bound cv_scores \

## 1 -42.6185 19.0465 [-23.5582499971, -41.8215743748, -73.993608929...

## 2 -36.0651 16.3184 [-18.002498199, -40.1507894517, -56.5286659068...

## 3 -34.1001 20.87 [-9.43012884381, -25.9584955394, -36.184188174...

## 4 -33.7681 20.1638 [-8.86076528781, -28.650217633, -35.7246353855...

## 5 -33.6392 20.5271 [-8.90807628524, -28.0684679108, -35.827463022...

## 6 -33.6276 19.0859 [-9.549485942, -30.9724602876, -32.6689523347,...

## 7 -32.4082 19.1455 [-10.0177149635, -28.3780298492, -30.926917231...

## 8 -32.3697 18.533 [-11.1431684243, -27.5765510172, -31.168994094...

## 9 -32.4016 21.5561 [-10.8972555995, -25.739780653, -30.1837430353...

## 10 -32.8504 22.6508 [-12.3909282079, -22.1533250755, -33.385407342...

## 11 -34.1065 24.7019 [-12.6429253721, -22.1676650245, -33.956999528...

## 12 -35.5814 25.693 [-12.7303397453, -25.0145323483, -34.211898373...

## 13 -37.1318 23.2657 [-12.4603005692, -26.0486211062, -33.074137979...

##

## feature_idx std_dev std_err

## 1 (12,) 18.9042 9.45212

## 2 (10, 12) 16.1965 8.09826

## 3 (10, 12, 5) 20.7142 10.3571

## 4 (10, 3, 12, 5) 20.0132 10.0066

## 5 (0, 10, 3, 12, 5) 20.3738 10.1869

## 6 (0, 3, 5, 7, 10, 12) 18.9433 9.47167

## 7 (0, 2, 3, 5, 7, 10, 12) 19.0026 9.50128

## 8 (0, 1, 2, 3, 5, 7, 10, 12) 18.3946 9.19731

## 9 (0, 1, 2, 3, 5, 7, 10, 11, 12) 21.3952 10.6976

## 10 (0, 1, 2, 3, 4, 5, 7, 10, 11, 12) 22.4816 11.2408

## 11 (0, 1, 2, 3, 4, 5, 6, 7, 10, 11, 12) 24.5175 12.2587

## 12 (0, 1, 2, 3, 4, 5, 6, 7, 9, 10, 11, 12) 25.5012 12.7506

## 13 (0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12) 23.0919 11.546

## No of features= 7

## [0, 2, 3, 5, 7, 10, 12]

## #################################################################################

## Features selected in forward fit

## Index([u'crimeRate', u'indus', u'chasRiver', u'rooms', u'distances',

## u'teacherRatio', u'status'],

## dtype='object')

1.3 Backward Fit

Backward fit belongs to the class of greedy algorithms which tries to optimize the feature set, by dropping a feature at every stage which results in the worst performance for a given criteria of Adj RSquared, Cp, BIC or AIC. For a dataset with features f1,f2,f3…fn, the backward fit starts with the all the features f1,f2.. fn to begin with. It then pick the ML model with a n-1 features by dropping the feature, , for e.g., the inclusion of which results in the worst performance in adj Rsquared, or minimum Cp, BIC or some such criteria. At every step 1 feature is dopped. There is no guarantee that the final list of features chosen will be the best among the lot. The computation required for this is of which is of the order of . Though backward fit is a sub optimal solution it is far more computationally efficient than best fit

, for e.g., the inclusion of which results in the worst performance in adj Rsquared, or minimum Cp, BIC or some such criteria. At every step 1 feature is dopped. There is no guarantee that the final list of features chosen will be the best among the lot. The computation required for this is of which is of the order of . Though backward fit is a sub optimal solution it is far more computationally efficient than best fit

1.3a Backward fit – R code

library(dplyr)

df=read.csv("Boston.csv",stringsAsFactors = FALSE)

names(df) <-c("no","crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

df1 <- df %>% dplyr::select("crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

set.seed(6)

nvmax<-13

cvError <- NULL

for(i in 1:nvmax){

noFolds=5

folds = sample(1:noFolds, nrow(df1), replace=TRUE)

cv<-0

for(j in 1:noFolds){

train <- df1[folds!=j,]

test <- df1[folds==j,]

fitFwd=regsubsets(cost~.,data=train,nvmax=13,method="backward")

coefi=coef(fitFwd,id=i)

test.mat=model.matrix(cost~.,data=test)

pred=test.mat[,names(coefi)]%*%coefi

rss=mean((test$cost - pred)^2)

cv=cv+rss

}

cvError[i]=cv/noFolds

}

a <- seq(1,13)

d <- as.data.frame(t(rbind(a,cvError)))

names(d) <- c("Features","CVError")

ggplot(d,aes(x=Features,y=CVError),color="blue") + geom_point() + geom_line(color="blue") +

xlab("No of features") + ylab("Cross Validation Error") +

ggtitle("Backward Selection - Cross Valdation Error vs No of Features")

![]()

a=which.min(cvError)

print(a)

## [1] 13

coefi=coef(fitFwd,id=a)

coefi

## (Intercept) crimeRate zone indus charles

## 36.650645380 -0.107980979 0.056237669 0.027016678 4.270631466

## nox rooms age distances highways

## -19.000715500 3.714720418 0.019952654 -1.472533973 0.326758004

## tax teacherRatio color status

## -0.011380750 -0.972862622 0.009549938 -0.582159093

Backward selection in R also indicates the 13 features and the corresponding coefficients as providing the best fit

1.3b Backward fit – Python code

The Backward Fit in Python uses the Sequential feature selection (SFS) package (SFS)(https://rasbt.github.io/mlxtend/user_guide/feature_selection/SequentialFeatureSelector/)

import numpy as np

import pandas as pd

import os

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression

from mlxtend.plotting import plot_sequential_feature_selection as plot_sfs

import matplotlib.pyplot as plt

from mlxtend.feature_selection import SequentialFeatureSelector as SFS

from sklearn.linear_model import LinearRegression

df = pd.read_csv("Boston.csv",encoding = "ISO-8859-1")

df.columns=["no","crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status","cost"]

X=df[["crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status"]]

y=df['cost']

lr = LinearRegression()

sfs = SFS(lr,

k_features=(1,13),

forward=False,

floating=False,

scoring='neg_mean_squared_error',

cv=5)

sfs = sfs.fit(X.as_matrix(), y.as_matrix())

a=sfs.get_metric_dict()

n=[]

o=[]

for i in np.arange(1,13):

n.append(-np.mean(a[i]['cv_scores']))

m=np.arange(1,13)

fig2=plt.plot(m,n)

fig2=plt.title('Mean CV Scores vs No of features')

fig2.figure.savefig('fig2.png', bbox_inches='tight')

print(pd.DataFrame.from_dict(sfs.get_metric_dict(confidence_interval=0.90)).T)

idx = np.argmin(n)

print "No of features=",idx

b=list(a[idx]['feature_idx'])

print("Features selected in bacward fit")

print(X.columns[b])

## avg_score ci_bound cv_scores \

## 1 -42.6185 19.0465 [-23.5582499971, -41.8215743748, -73.993608929...

## 2 -36.0651 16.3184 [-18.002498199, -40.1507894517, -56.5286659068...

## 3 -35.4992 13.9619 [-17.2329292677, -44.4178648308, -51.633177846...

## 4 -33.463 12.4081 [-20.6415333292, -37.3247852146, -47.479302977...

## 5 -33.1038 10.6156 [-20.2872309863, -34.6367078466, -45.931870352...

## 6 -32.0638 10.0933 [-19.4463829372, -33.460638577, -42.726257249,...

## 7 -30.7133 9.23881 [-19.4425181917, -31.1742902259, -40.531266671...

## 8 -29.7432 9.84468 [-19.445277268, -30.0641187173, -40.2561247122...

## 9 -29.0878 9.45027 [-19.3545569877, -30.094768669, -39.7506036377...

## 10 -28.9225 9.39697 [-18.562171585, -29.968504938, -39.9586835965,...

## 11 -29.4301 10.8831 [-18.3346152225, -30.3312847532, -45.065432793...

## 12 -30.4589 11.1486 [-18.493389527, -35.0290639374, -45.1558231765...

## 13 -37.1318 23.2657 [-12.4603005692, -26.0486211062, -33.074137979...

##

## feature_idx std_dev std_err

## 1 (12,) 18.9042 9.45212

## 2 (10, 12) 16.1965 8.09826

## 3 (10, 12, 7) 13.8576 6.92881

## 4 (12, 10, 4, 7) 12.3154 6.15772

## 5 (4, 7, 8, 10, 12) 10.5363 5.26816

## 6 (4, 7, 8, 9, 10, 12) 10.0179 5.00896

## 7 (1, 4, 7, 8, 9, 10, 12) 9.16981 4.58491

## 8 (1, 4, 7, 8, 9, 10, 11, 12) 9.77116 4.88558

## 9 (0, 1, 4, 7, 8, 9, 10, 11, 12) 9.37969 4.68985

## 10 (0, 1, 4, 6, 7, 8, 9, 10, 11, 12) 9.3268 4.6634

## 11 (0, 1, 3, 4, 6, 7, 8, 9, 10, 11, 12) 10.8018 5.40092

## 12 (0, 1, 2, 3, 4, 6, 7, 8, 9, 10, 11, 12) 11.0653 5.53265

## 13 (0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12) 23.0919 11.546

## No of features= 9

## Features selected in bacward fit

## Index([u'crimeRate', u'zone', u'NO2', u'distances', u'idxHighways', u'taxRate',

## u'teacherRatio', u'color', u'status'],

## dtype='object')

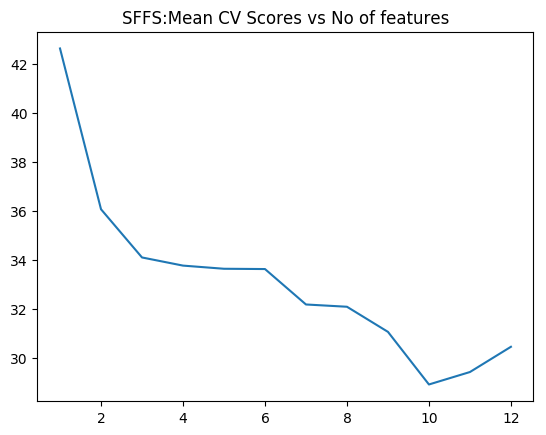

1.3c Sequential Floating Forward Selection (SFFS) – Python code

The Sequential Feature search also includes ‘floating’ variants which include or exclude features conditionally, once they were excluded or included. The SFFS can conditionally include features which were excluded from the previous step, if it results in a better fit. This option will tend to a better solution, than plain simple SFS. These variants are included below

import numpy as np

import pandas as pd

import os

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression

from sklearn.datasets import load_boston

from mlxtend.plotting import plot_sequential_feature_selection as plot_sfs

import matplotlib.pyplot as plt

from mlxtend.feature_selection import SequentialFeatureSelector as SFS

from sklearn.linear_model import LinearRegression

df = pd.read_csv("Boston.csv",encoding = "ISO-8859-1")

df.columns=["no","crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status","cost"]

X=df[["crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status"]]

y=df['cost']

lr = LinearRegression()

sffs = SFS(lr,

k_features=(1,13),

forward=True,

floating=True,

scoring='neg_mean_squared_error',

cv=5)

sffs = sffs.fit(X.as_matrix(), y.as_matrix())

a=sffs.get_metric_dict()

n=[]

o=[]

for i in np.arange(1,13):

n.append(-np.mean(a[i]['cv_scores']))

m=np.arange(1,13)

fig3=plt.plot(m,n)

fig3=plt.title('SFFS:Mean CV Scores vs No of features')

fig3.figure.savefig('fig3.png', bbox_inches='tight')

print(pd.DataFrame.from_dict(sffs.get_metric_dict(confidence_interval=0.90)).T)

idx = np.argmin(n)

print "No of features=",idx

b=list(a[idx]['feature_idx'])

print(b)

print("#################################################################################")

print("Features selected in forward fit")

print(X.columns[b])

## avg_score ci_bound cv_scores \

## 1 -42.6185 19.0465 [-23.5582499971, -41.8215743748, -73.993608929...

## 2 -36.0651 16.3184 [-18.002498199, -40.1507894517, -56.5286659068...

## 3 -34.1001 20.87 [-9.43012884381, -25.9584955394, -36.184188174...

## 4 -33.7681 20.1638 [-8.86076528781, -28.650217633, -35.7246353855...

## 5 -33.6392 20.5271 [-8.90807628524, -28.0684679108, -35.827463022...

## 6 -33.6276 19.0859 [-9.549485942, -30.9724602876, -32.6689523347,...

## 7 -32.1834 12.1001 [-17.9491036167, -39.6479234651, -45.470227740...

## 8 -32.0908 11.8179 [-17.4389015788, -41.2453629843, -44.247557798...

## 9 -31.0671 10.1581 [-17.2689542913, -37.4379370429, -41.366372300...

## 10 -28.9225 9.39697 [-18.562171585, -29.968504938, -39.9586835965,...

## 11 -29.4301 10.8831 [-18.3346152225, -30.3312847532, -45.065432793...

## 12 -30.4589 11.1486 [-18.493389527, -35.0290639374, -45.1558231765...

## 13 -37.1318 23.2657 [-12.4603005692, -26.0486211062, -33.074137979...

##

## feature_idx std_dev std_err

## 1 (12,) 18.9042 9.45212

## 2 (10, 12) 16.1965 8.09826

## 3 (10, 12, 5) 20.7142 10.3571

## 4 (10, 3, 12, 5) 20.0132 10.0066

## 5 (0, 10, 3, 12, 5) 20.3738 10.1869

## 6 (0, 3, 5, 7, 10, 12) 18.9433 9.47167

## 7 (0, 1, 2, 3, 7, 10, 12) 12.0097 6.00487

## 8 (0, 1, 2, 3, 7, 8, 10, 12) 11.7297 5.86484

## 9 (0, 1, 2, 3, 7, 8, 9, 10, 12) 10.0822 5.04111

## 10 (0, 1, 4, 6, 7, 8, 9, 10, 11, 12) 9.3268 4.6634

## 11 (0, 1, 3, 4, 6, 7, 8, 9, 10, 11, 12) 10.8018 5.40092

## 12 (0, 1, 2, 3, 4, 6, 7, 8, 9, 10, 11, 12) 11.0653 5.53265

## 13 (0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12) 23.0919 11.546

## No of features= 9

## [0, 1, 2, 3, 7, 8, 9, 10, 12]

## #################################################################################

## Features selected in forward fit

## Index([u'crimeRate', u'zone', u'indus', u'chasRiver', u'distances',

## u'idxHighways', u'taxRate', u'teacherRatio', u'status'],

## dtype='object')

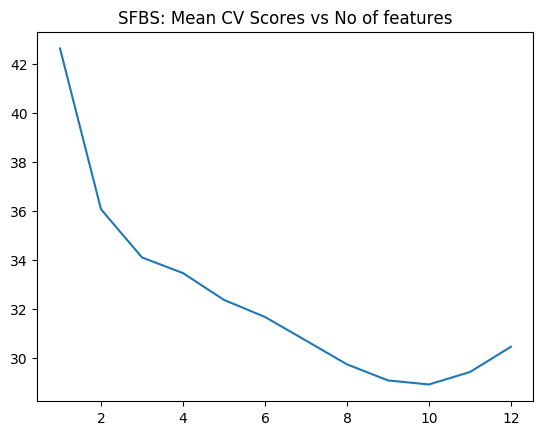

1.3d Sequential Floating Backward Selection (SFBS) – Python code

The SFBS is an extension of the SBS. Here features that are excluded at any stage can be conditionally included if the resulting feature set gives a better fit.

import numpy as np

import pandas as pd

import os

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression

from sklearn.datasets import load_boston

from mlxtend.plotting import plot_sequential_feature_selection as plot_sfs

import matplotlib.pyplot as plt

from mlxtend.feature_selection import SequentialFeatureSelector as SFS

from sklearn.linear_model import LinearRegression

df = pd.read_csv("Boston.csv",encoding = "ISO-8859-1")

df.columns=["no","crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status","cost"]

X=df[["crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status"]]

y=df['cost']

lr = LinearRegression()

sffs = SFS(lr,

k_features=(1,13),

forward=False,

floating=True,

scoring='neg_mean_squared_error',

cv=5)

sffs = sffs.fit(X.as_matrix(), y.as_matrix())

a=sffs.get_metric_dict()

n=[]

o=[]

for i in np.arange(1,13):

n.append(-np.mean(a[i]['cv_scores']))

m=np.arange(1,13)

fig4=plt.plot(m,n)

fig4=plt.title('SFBS: Mean CV Scores vs No of features')

fig4.figure.savefig('fig4.png', bbox_inches='tight')

print(pd.DataFrame.from_dict(sffs.get_metric_dict(confidence_interval=0.90)).T)

idx = np.argmin(n)

print "No of features=",idx

b=list(a[idx]['feature_idx'])

print(b)

print("#################################################################################")

print("Features selected in backward floating fit")

print(X.columns[b])

## avg_score ci_bound cv_scores \

## 1 -42.6185 19.0465 [-23.5582499971, -41.8215743748, -73.993608929...

## 2 -36.0651 16.3184 [-18.002498199, -40.1507894517, -56.5286659068...

## 3 -34.1001 20.87 [-9.43012884381, -25.9584955394, -36.184188174...

## 4 -33.463 12.4081 [-20.6415333292, -37.3247852146, -47.479302977...

## 5 -32.3699 11.2725 [-20.8771078371, -34.9825657934, -45.813447203...

## 6 -31.6742 11.2458 [-20.3082500364, -33.2288990522, -45.535507868...

## 7 -30.7133 9.23881 [-19.4425181917, -31.1742902259, -40.531266671...

## 8 -29.7432 9.84468 [-19.445277268, -30.0641187173, -40.2561247122...

## 9 -29.0878 9.45027 [-19.3545569877, -30.094768669, -39.7506036377...

## 10 -28.9225 9.39697 [-18.562171585, -29.968504938, -39.9586835965,...

## 11 -29.4301 10.8831 [-18.3346152225, -30.3312847532, -45.065432793...

## 12 -30.4589 11.1486 [-18.493389527, -35.0290639374, -45.1558231765...

## 13 -37.1318 23.2657 [-12.4603005692, -26.0486211062, -33.074137979...

##

## feature_idx std_dev std_err

## 1 (12,) 18.9042 9.45212

## 2 (10, 12) 16.1965 8.09826

## 3 (10, 12, 5) 20.7142 10.3571

## 4 (4, 10, 7, 12) 12.3154 6.15772

## 5 (12, 10, 4, 1, 7) 11.1883 5.59417

## 6 (4, 7, 8, 10, 11, 12) 11.1618 5.58088

## 7 (1, 4, 7, 8, 9, 10, 12) 9.16981 4.58491

## 8 (1, 4, 7, 8, 9, 10, 11, 12) 9.77116 4.88558

## 9 (0, 1, 4, 7, 8, 9, 10, 11, 12) 9.37969 4.68985

## 10 (0, 1, 4, 6, 7, 8, 9, 10, 11, 12) 9.3268 4.6634

## 11 (0, 1, 3, 4, 6, 7, 8, 9, 10, 11, 12) 10.8018 5.40092

## 12 (0, 1, 2, 3, 4, 6, 7, 8, 9, 10, 11, 12) 11.0653 5.53265

## 13 (0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12) 23.0919 11.546

## No of features= 9

## [0, 1, 4, 7, 8, 9, 10, 11, 12]

## #################################################################################

## Features selected in backward floating fit

## Index([u'crimeRate', u'zone', u'NO2', u'distances', u'idxHighways', u'taxRate',

## u'teacherRatio', u'color', u'status'],

## dtype='object')

1.4 Ridge regression

In Linear Regression the Residual Sum of Squares (RSS) is given as

Ridge regularization =

where is the regularization or tuning parameter. Increasing increases the penalty on the coefficients thus shrinking them. However in Ridge Regression features that do not influence the target variable will shrink closer to zero but never become zero except for very large values of

Ridge regression in R requires the ‘glmnet’ package

1.4a Ridge Regression – R code

library(glmnet)

library(dplyr)

df=read.csv("Boston.csv",stringsAsFactors = FALSE)

names(df) <-c("no","crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

df1 <- df %>% dplyr::select("crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

X=as.matrix(df1[,1:13])

y=df1$cost

fitRidge <-glmnet(X,y,alpha=0)

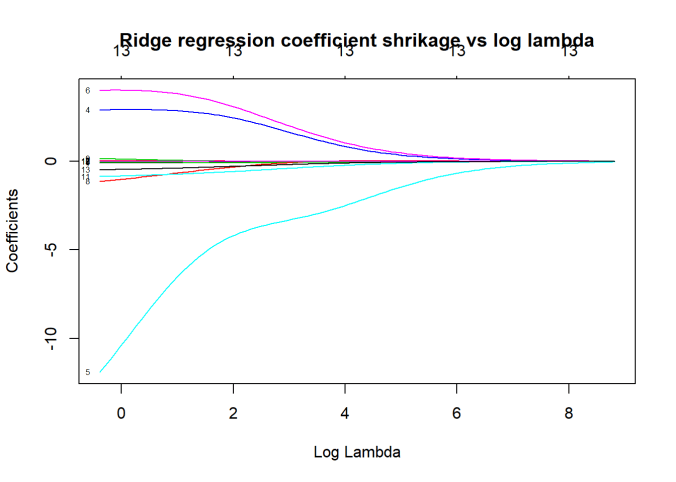

plot(fitRidge,xvar="lambda",label=TRUE,main= "Ridge regression coefficient shrikage vs log lambda")

![]() The plot below shows how the 13 coefficients for the 13 predictors vary when lambda is increased. The x-axis includes log (lambda). We can see that increasing lambda from

The plot below shows how the 13 coefficients for the 13 predictors vary when lambda is increased. The x-axis includes log (lambda). We can see that increasing lambda from  to

to  significantly shrinks the coefficients. We can draw a vertical line from the x-axis and read the values of the 13 coefficients. Some of them will be close to zero

significantly shrinks the coefficients. We can draw a vertical line from the x-axis and read the values of the 13 coefficients. Some of them will be close to zero

cvRidge=cv.glmnet(X,y,alpha=0)

plot(cvRidge, main="Ridge regression Cross Validation Error (10 fold)")

![]() This gives the 10 fold Cross Validation Error with respect to log (lambda) As lambda increase the MSE increases

This gives the 10 fold Cross Validation Error with respect to log (lambda) As lambda increase the MSE increases

1.4a Ridge Regression – Python code

The coefficient shrinkage for Python can be plotted like R using Least Angle Regression model a.k.a. LARS package. This is included below

import numpy as np

import pandas as pd

import os

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

df = pd.read_csv("Boston.csv",encoding = "ISO-8859-1")

df.columns=["no","crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status","cost"]

X=df[["crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status"]]

y=df['cost']

from sklearn.preprocessing import MinMaxScaler

scaler = MinMaxScaler()

from sklearn.linear_model import Ridge

X_train, X_test, y_train, y_test = train_test_split(X, y,

random_state = 0)

X_train_scaled = scaler.fit_transform(X_train)

X_test_scaled = scaler.transform(X_test)

linridge = Ridge(alpha=20.0).fit(X_train_scaled, y_train)

print('R-squared score (training): {:.3f}'

.format(linridge.score(X_train_scaled, y_train)))

print('R-squared score (test): {:.3f}'

.format(linridge.score(X_test_scaled, y_test)))

print('Number of non-zero features: {}'

.format(np.sum(linridge.coef_ != 0)))

trainingRsquared=[]

testRsquared=[]

print('Ridge regression: effect of alpha regularization parameter\n')

for this_alpha in [0.001,.01,.1,0, 1, 10, 20, 50, 100, 1000]:

linridge = Ridge(alpha = this_alpha).fit(X_train_scaled, y_train)

r2_train = linridge.score(X_train_scaled, y_train)

r2_test = linridge.score(X_test_scaled, y_test)

num_coeff_bigger = np.sum(abs(linridge.coef_) > 1.0)

trainingRsquared.append(r2_train)

testRsquared.append(r2_test)

alpha=[0.001,.01,.1,0, 1, 10, 20, 50, 100, 1000]

trainingRsquared=pd.DataFrame(trainingRsquared,index=alpha)

testRsquared=pd.DataFrame(testRsquared,index=alpha)

df3=pd.concat([trainingRsquared,testRsquared],axis=1)

df3.columns=['trainingRsquared','testRsquared']

fig5=df3.plot()

fig5=plt.title('Ridge training and test squared error vs Alpha')

fig5.figure.savefig('fig5.png', bbox_inches='tight')

from sklearn import linear_model

n_alphas = 200

alphas = np.logspace(0, 8, n_alphas)

coefs = []

for a in alphas:

ridge = linear_model.Ridge(alpha=a, fit_intercept=False)

ridge.fit(X_train_scaled, y_train)

coefs.append(ridge.coef_)

ax = plt.gca()

fig6=ax.plot(alphas, coefs)

fig6=ax.set_xscale('log')

fig6=ax.set_xlim(ax.get_xlim()[::-1])

fig6=plt.xlabel('alpha')

fig6=plt.ylabel('weights')

fig6=plt.title('Ridge coefficients as a function of the regularization')

fig6=plt.axis('tight')

plt.savefig('fig6.png', bbox_inches='tight')

## R-squared score (training): 0.620

## R-squared score (test): 0.438

## Number of non-zero features: 13

## Ridge regression: effect of alpha regularization parameter

![]()

![]() The plot below shows the training and test error when increasing the tuning or regularization parameter ‘alpha’

The plot below shows the training and test error when increasing the tuning or regularization parameter ‘alpha’

For Python the coefficient shrinkage with LARS must be viewed from right to left, where you have increasing alpha. As alpha increases the coefficients shrink to 0.

1.5 Lasso regularization

The Lasso is another form of regularization, also known as L1 regularization. Unlike the Ridge Regression where the coefficients of features which do not influence the target tend to zero, in the lasso regualrization the coefficients become 0. The general form of Lasso is as follows

1.5a Lasso regularization – R code

library(glmnet)

library(dplyr)

df=read.csv("Boston.csv",stringsAsFactors = FALSE)

names(df) <-c("no","crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

df1 <- df %>% dplyr::select("crimeRate","zone","indus","charles","nox","rooms","age",

"distances","highways","tax","teacherRatio","color","status","cost")

X=as.matrix(df1[,1:13])

y=df1$cost

fitLasso <- glmnet(X,y)

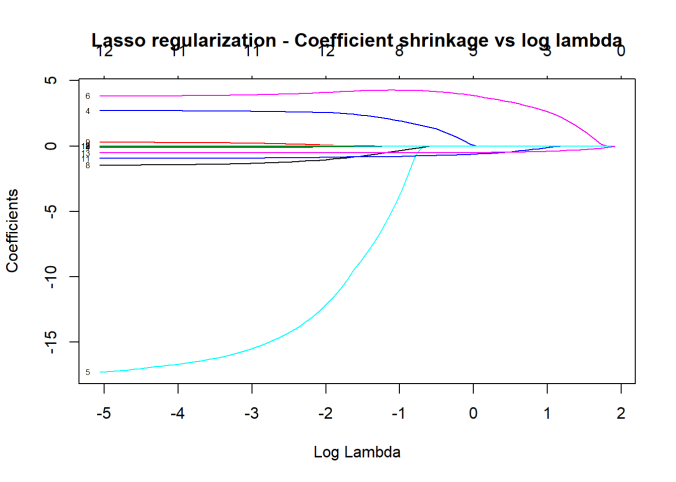

plot(fitLasso,xvar="lambda",label=TRUE,main="Lasso regularization - Coefficient shrinkage vs log lambda")

![]() The plot below shows that in L1 regularization the coefficients actually become zero with increasing lambda

The plot below shows that in L1 regularization the coefficients actually become zero with increasing lambda

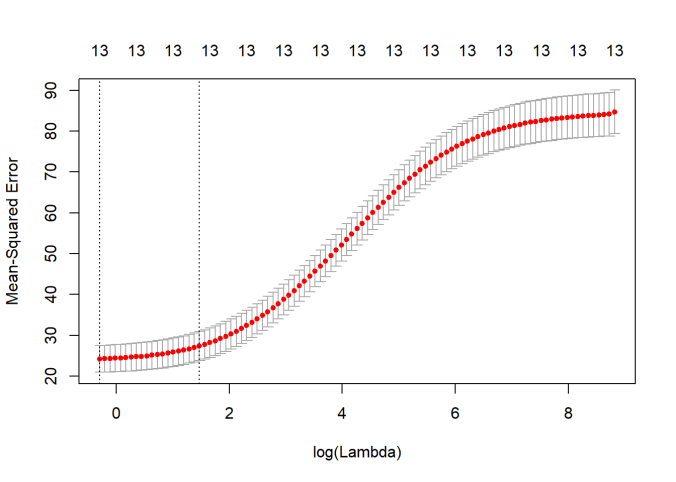

cvLasso=cv.glmnet(X,y,alpha=0)

plot(cvLasso)

![]() This gives the MSE for the lasso model

This gives the MSE for the lasso model

1.5 b Lasso regularization – Python code

import numpy as np

import pandas as pd

import os

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

from sklearn.linear_model import Lasso

from sklearn.preprocessing import MinMaxScaler

from sklearn import linear_model

scaler = MinMaxScaler()

df = pd.read_csv("Boston.csv",encoding = "ISO-8859-1")

#Rename the columns

df.columns=["no","crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status","cost"]

X=df[["crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status"]]

y=df['cost']

X_train, X_test, y_train, y_test = train_test_split(X, y,

random_state = 0)

X_train_scaled = scaler.fit_transform(X_train)

X_test_scaled = scaler.transform(X_test)

linlasso = Lasso(alpha=0.1, max_iter = 10).fit(X_train_scaled, y_train)

print('Non-zero features: {}'

.format(np.sum(linlasso.coef_ != 0)))

print('R-squared score (training): {:.3f}'

.format(linlasso.score(X_train_scaled, y_train)))

print('R-squared score (test): {:.3f}\n'

.format(linlasso.score(X_test_scaled, y_test)))

print('Features with non-zero weight (sorted by absolute magnitude):')

for e in sorted (list(zip(list(X), linlasso.coef_)),

key = lambda e: -abs(e[1])):

if e[1] != 0:

print('\t{}, {:.3f}'.format(e[0], e[1]))

print('Lasso regression: effect of alpha regularization\n\

parameter on number of features kept in final model\n')

trainingRsquared=[]

testRsquared=[]

#for alpha in [0.01,0.05,0.1, 1, 2, 3, 5, 10, 20, 50]:

for alpha in [0.01,0.07,0.05, 0.1, 1,2, 3, 5, 10]:

linlasso = Lasso(alpha, max_iter = 10000).fit(X_train_scaled, y_train)

r2_train = linlasso.score(X_train_scaled, y_train)

r2_test = linlasso.score(X_test_scaled, y_test)

trainingRsquared.append(r2_train)

testRsquared.append(r2_test)

alpha=[0.01,0.07,0.05, 0.1, 1,2, 3, 5, 10]

#alpha=[0.01,0.05,0.1, 1, 2, 3, 5, 10, 20, 50]

trainingRsquared=pd.DataFrame(trainingRsquared,index=alpha)

testRsquared=pd.DataFrame(testRsquared,index=alpha)

df3=pd.concat([trainingRsquared,testRsquared],axis=1)

df3.columns=['trainingRsquared','testRsquared']

fig7=df3.plot()

fig7=plt.title('LASSO training and test squared error vs Alpha')

fig7.figure.savefig('fig7.png', bbox_inches='tight')

## Non-zero features: 7

## R-squared score (training): 0.726

## R-squared score (test): 0.561

##

## Features with non-zero weight (sorted by absolute magnitude):

## status, -18.361

## rooms, 18.232

## teacherRatio, -8.628

## taxRate, -2.045

## color, 1.888

## chasRiver, 1.670

## distances, -0.529

## Lasso regression: effect of alpha regularization

## parameter on number of features kept in final model

##

## Computing regularization path using the LARS ...

## .C:\Users\Ganesh\ANACON~1\lib\site-packages\sklearn\linear_model\coordinate_descent.py:484: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Fitting data with very small alpha may cause precision problems.

## ConvergenceWarning)

1.5c Lasso coefficient shrinkage – Python code

To plot the coefficient shrinkage for Lasso the Least Angle Regression model a.k.a. LARS package. This is shown below

import numpy as np

import pandas as pd

import os

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

from sklearn.linear_model import Lasso

from sklearn.preprocessing import MinMaxScaler

from sklearn import linear_model

scaler = MinMaxScaler()

df = pd.read_csv("Boston.csv",encoding = "ISO-8859-1")

df.columns=["no","crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status","cost"]

X=df[["crimeRate","zone","indus","chasRiver","NO2","rooms","age",

"distances","idxHighways","taxRate","teacherRatio","color","status"]]

y=df['cost']

X_train, X_test, y_train, y_test = train_test_split(X, y,

random_state = 0)

X_train_scaled = scaler.fit_transform(X_train)

X_test_scaled = scaler.transform(X_test)

print("Computing regularization path using the LARS ...")

alphas, _, coefs = linear_model.lars_path(X_train_scaled, y_train, method='lasso', verbose=True)

xx = np.sum(np.abs(coefs.T), axis=1)

xx /= xx[-1]

fig8=plt.plot(xx, coefs.T)

ymin, ymax = plt.ylim()

fig8=plt.vlines(xx, ymin, ymax, linestyle='dashed')

fig8=plt.xlabel('|coef| / max|coef|')

fig8=plt.ylabel('Coefficients')

fig8=plt.title('LASSO Path - Coefficient Shrinkage vs L1')

fig8=plt.axis('tight')

plt.savefig('fig8.png', bbox_inches='tight')

This 3rd part of the series covers the main ‘feature selection’ methods. I hope these posts serve as a quick and useful reference to ML code both for R and Python!

Stay tuned for further updates to this series!

Watch this space!

You may also like

1. Natural language processing: What would Shakespeare say?

2. Introducing QCSimulator: A 5-qubit quantum computing simulator in R

3. GooglyPlus: yorkr analyzes IPL players, teams, matches with plots and tables

4. My travels through the realms of Data Science, Machine Learning, Deep Learning and (AI)

5. Experiments with deblurring using OpenCV

6. R vs Python: Different similarities and similar differences

To see all posts see Index of posts

scales the dot product so that the dot product values are not overly large

scales the dot product so that the dot product values are not overly large

and

and  are the weight matrices, and

are the weight matrices, and  and

and  are the biases

are the biases  x

x  and

and x

x  and

and  is the activation function which can be ReLU, GELU or SwiGLU

is the activation function which can be ReLU, GELU or SwiGLU

,

,  ,

,  . By multiplyting these matrices with the input vectors we get Q,K and V vectors. The attention is computed as

. By multiplyting these matrices with the input vectors we get Q,K and V vectors. The attention is computed as

,

,

= 64

= 64

Checkout my book ‘Deep Learning from first principles: Second Edition – In vectorized Python, R and Octave’. My book starts with the implementation of a simple 2-layer Neural Network and works its way to a generic L-Layer Deep Learning Network, with all the bells and whistles. The derivations have been discussed in detail. The code has been extensively commented and included in its entirety in the Appendix sections. My book is available on Amazon as

Checkout my book ‘Deep Learning from first principles: Second Edition – In vectorized Python, R and Octave’. My book starts with the implementation of a simple 2-layer Neural Network and works its way to a generic L-Layer Deep Learning Network, with all the bells and whistles. The derivations have been discussed in detail. The code has been extensively commented and included in its entirety in the Appendix sections. My book is available on Amazon as

In this book I implement some of the most common, but important Machine Learning algorithms in R and equivalent Python code.

In this book I implement some of the most common, but important Machine Learning algorithms in R and equivalent Python code.

ML models have to be searched. This can be shown as follows

ML models have to be searched. This can be shown as follows ways to choose single feature ML models among ‘n’ features,

ways to choose single feature ML models among ‘n’ features,  ways to choose 2 feature models among ‘n’ models and so on, or

ways to choose 2 feature models among ‘n’ models and so on, or

models to search amongst in Best Fit. For 10 features this is

models to search amongst in Best Fit. For 10 features this is  or ~1000 models and for 40 features this becomes

or ~1000 models and for 40 features this becomes  which almost 1 trillion. Usually there are datasets with 1000 or maybe even 100000 features and Best fit becomes computationally infeasible.

which almost 1 trillion. Usually there are datasets with 1000 or maybe even 100000 features and Best fit becomes computationally infeasible. models

models

Then felt I like some watcher of the skies

Then felt I like some watcher of the skies